How do stock exchange listing rules evolve? Evidence from the London Stock Exchange’s Alternative Investment Market (AIM), 1995-2025

Posted:

Time to read:

2 Minutes

The London Stock Exchange’s Alternative Investment Market (AIM), a stock exchange for growth companies, is undergoing a regulatory ‘reset’ to try and overcome a host of challenges that have contributed to a shrinking market that has lost more than 1,000 listed companies over the past two decades (LSE Discussion Paper, Nov 2025). But before considering how AIM should evolve in the future, it is worth asking: how has it evolved in the past?

Three highlights of how the AIM listing rules have evolved

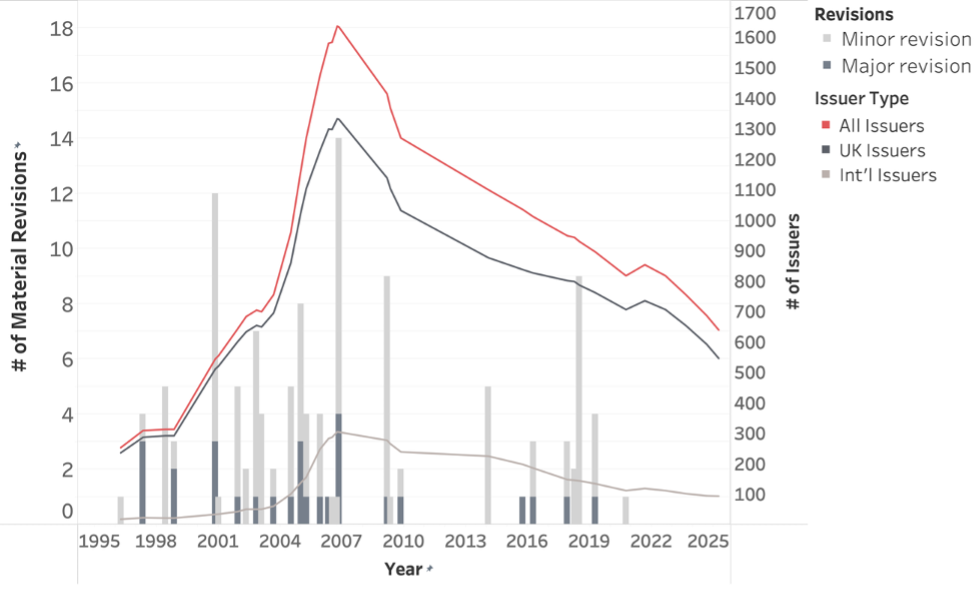

First, the AIM listing rules1 evolve much more during the first 12 years (1995-2007) than the next 18 years (2007-2025). More than two-thirds of material rule revisions occur during the initial 12 years of AIM’s history, with more consequential revisions decreasing over time. As Figure 1 below displays, the rules are revised more frequently as the number of issuers and market participants grows until an all-time high in 2007, after which fewer revisions occur as the number of issuers declines steadily.

Figure 1: AIM Rule Revisions and Number of Issuers, 1995-2025

This pattern is consistent with explanations of rule evolution related to regulatory demand (where rule production is influenced by demand) as well as regulatory learning (where the regulator acquires rule-making expertise over time, and as the rules become more fit for purpose fewer revisions are necessary).

Second, there are there are relatively long periods of regulatory stasis (periods without rule revisions) in the years after 2007, with no evolution in the AIM listing rules from February 2010 to May 2014 and January 2021 to the July 2025. This can partly be explained as a feature of principles-based regulatory systems, whereby market practice can meaningfully change depending on how the rule-maker exercises discretion. This could also be explained by increasing risk aversion from the rule-maker, the London Stock Exchange plc (Exchange), which operates AIM and writes and enforces the AIM listing rules. Evidence is only found for two ‘regulatory shocks’ during the periods of regulatory stasis after 2007, which provides only limited support for a punctuated equilibria explanation of rule evolution, whereby shocks such as economic or political crises cause legal rules to evolve (Roe 1996).

Third, while the AIM listing rules have increased nine times in length since inception, the main drivers of expansion have been in the AIM Disciplinary and Appeals Handbook and targeted rules for investing companies (eg, SPACs) and resource companies; the core regulatory framework has not evolved as drastically as the number of minor revisions might suggest. However, the cumulative effect of minor revisions and expanding guidance notes is consistent with concerns raised by market participants of an increasing regulatory burden for AIM companies.

A suggestion for AIM going forward

Much of the recent focus has been on specific proposals to revise the AIM listing rules—trade associations like the Quoted Companies Alliance have submitted thoughtful feedback, and the Exchange’s November 2025 regulatory proposals are a step in the right direction. However, this research suggests that it is not just the content of the forthcoming regulatory reforms that counts, but also how the rules and guidance will be interpreted and how frequently they will be revised thereafter. Acutely risk-averse interpretations of the AIM listing rules by the Exchange can undermine the benefits of flexible, principles-based regulation for smaller companies. The Exchange should be cognisant of the risks of ‘rule tinkering’, whereby minor revisions and expansions to the guidance notes may not immediately result in qualitatively substantial changes, but cumulatively may have a more significant long-term effect, potentially increasing regulatory costs and compliance obligations without proportionate benefits.

The full article is forthcoming in the Journal of Financial Regulation and can be found here.

Jonathan Chan is an Assistant Professor at McGill University Faculty of Law.

OBLB types:

Research

OBLB keywords:

London Stock Exchange

Self-regulation

Private ordering

Alternative Investment Market (AIM)

Stock exchange

Jurisdiction:

United Kingdom

Share: