Delegated Gatekeepers and a Case Study of the Alternative Investment Market (AIM)

Posted:

Time to read:

3 Minutes

Part I of this post presents ‘delegated gatekeeping’ as a refinement to conventional gatekeeper theory. Part II presents one of the most detailed studies of nominated advisers (Nomads) on AIM to date, suggesting that previous criticisms of AIM gatekeepers are no longer reflective of how the market has developed.

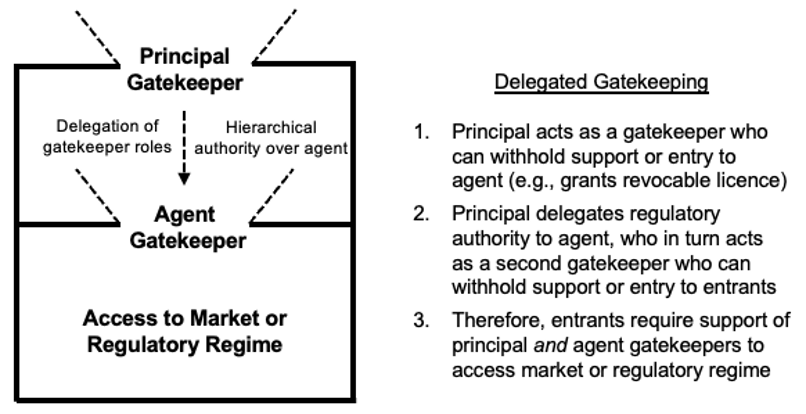

Part I (Theory): How does gatekeeping change when one gatekeeper delegates its roles to another?

When the UK Solicitors Regulation Authority (SRA) licenses lawyers, it delegates supervisory duties to fully qualified lawyers (‘training principals’), who must oversee trainee solicitors and certify that they possess certain competencies (SRA). In systems of ‘delegated gatekeeping’, a principal gatekeeper delegates revocable regulatory authority to agent gatekeepers, creating a hierarchical relationship between principal and agent. In practice, this means that a trainee solicitor requires the support of both the UK SRA and a training principal to enter the regulatory regime. A unique feature is that the training principal (as agent gatekeeper) is incentivized to perform gatekeeping roles without financial compensation because he or she is also subject to the regulatory authority of the principal gatekeeper. This permits a lower cost regulatory system overall, since the principal’s monitoring costs have decreased.

Delegated gatekeeping is not unique to lawyer licensing: consider regulatory bodies that certify architects or pilots in the UK and license certified public accountants in the US, provide ‘Energy Star’ certification in the US, or even stock exchange listing sponsors in the context of financial regulation.

When principal gatekeepers delegate their core functions to agent gatekeepers, agents take on new roles such as reputational stewardship (safeguarding the principal’s reputation), monitoring participants and whistleblowing (to minimise the risk of regulatory breach), and sharing regulatory authority with the principal (such as rule interpretation and enforcement).

FIGURE 1: Delegated Gatekeeping

Part II (Case Study): Why Nomads’ reputational incentives have improved on AIM

AIM has previously come under fire, in the height of its boom days surrounding 2007, for being ‘the limiting example of reliance on a gatekeeper’ (Coffee, 2006). This paper undertakes a fresh assessment of gatekeepers on AIM,[1] providing evidence of how Nomads’ reputational incentives have developed significantly since 2007, improving gatekeeping quality by ameliorating (not eliminating) their conflicts of interest relative to historical levels.

Consider the following evidence demonstrating that Nomads have stronger reputational incentives than compared to circa 2007:

- The number of Nomads decreased significantly between 2007-08 to 2025 (from at least 84 Nomads in 2007 to the low 20s in recent years). This allows for more effective monitoring by the Exchange and gives each Nomad more skin in the game.

- The vast majority of Nomads (75%+) also act as corporate brokers for their advisee companies. This increases the penalty for wrongdoing through the loss of corporate fundraising fees, which are much more lucrative than regulatory advisory fees.

- The majority of Nomads are locally based firms who derive most of their business in the City (London’s financial district), making them highly dependent on maintaining good standing with the Exchange.

- Nomads are bonded to the Exchange by interactions in parallel contexts outside of AIM, such as acting as listing sponsors on the LSE Main Market. The vast majority of Nomads (90% in 2025, up from 60% in 2021) are affiliates of firms that act as listing sponsors for premium-listed firms on the LSE Main Market.

- AIM has evolved towards a market that is much more reliant on secondary fundraising (seasoned offerings averaged 80% of funds raised from 2014-2024), rather than primary fundraising via IPOs. The increase in repeated interactions between investors and the same AIM companies strengthens reputational incentives.

- The Exchange began publicly censuring Nomads for wrongdoing in 2007, and publicly disciplined Nomads have soon gone out of business. This points to the strength of reputational sanctions.

In summary, the evidence suggests that gatekeeping on AIM has improved relative to historic levels (circa 2007) because reputational incentives have ameliorated Nomads’ conflicts of interests. However, this does not imply that conflicts have been sufficiently alleviated in absolute terms. The paper concludes with regulatory proposals to the AIM Rules for Companies that would improve governance and further curb conflicts.

Read the author’s article, forthcoming The Cambridge Law Journal.

Jonathan Chan is an Assistant Professor at McGill University Faculty of Law

Endnotes

[1] AIM-listed companies must retain a regulatory advisory firm called a ‘nominated adviser’ (Nomad) at all times. Nomads are agent gatekeepers that are licensed by the principal gatekeeper, the London Stock Exchange plc, which operates AIM. In essence, Nomads have four key functions: 1) certify and support companies’ appropriateness for AIM (at listing and thereafter); 2) act as reputational intermediary for AIM companies and reputational steward for the Exchange; 3) monitor advisee companies and report wrongdoing to the Exchange; and 4) act as a rule interpreter (for advisee companies) and rule enforcer (for the Exchange).

OBLB types:

Research

OBLB keywords:

Gatekeepers

Stock exchange

Self-regulation

London Stock Exchange

Alternative Investment Market (AIM)

Jurisdiction:

United Kingdom

Share: