Restructuring Argentina's Sovereign Debts - Navigating the Legal Labyrinth

Posted:

Time to read:

5 Minutes

For almost two years, Argentina has been facing a severe economic recession and has not had the ability to access international capital markets. This has left Argentina vulnerable to a sovereign debt crisis, and substantially increased the likelihood of a debt restructuring.

My new short paper on a potential Argentine sovereign debt restructuring has two objectives. First, it seeks to provide some insights into Argentina’s current financial situation by identifying and quantifying Argentina’s public debt obligations on the basis of Bloomberg data. Second, the paper sketches out some of the key legal challenges that the government is facing with regard to the restructuring of its different debt instruments. These challenges are likely to shape negotiations and define the perimeter of the debt workout.

Argentina’s Current Sovereign Debt Stock - An Overview

According to the latest government statistics, Argentina’s total outstanding debt totals $337 billion, or 80.7 percent of GDP (the amount varies depending on the peso-dollar exchange rate, since a relevant portion of such debt is short-term and denominated in pesos). Of the government’s total financial obligations, 58 percent are denominated in US dollars, 13.8 percent in Argentine pesos, 6.5 percent in euros, and 12.0 percent in other currencies (including the IMF’s Special Drawing Rights).

Domestic debt

23.2 percent of the total debt stock (excluding IMF loans) is denominated in domestic currency. Argentina has, according to Reuters, already delayed the repayment of some of its domestic debt. Domestic-currency debt is typically held by local residents and institutional investors, and, as I describe below, there are fewer legal risks associated with the restructuring of such obligations.

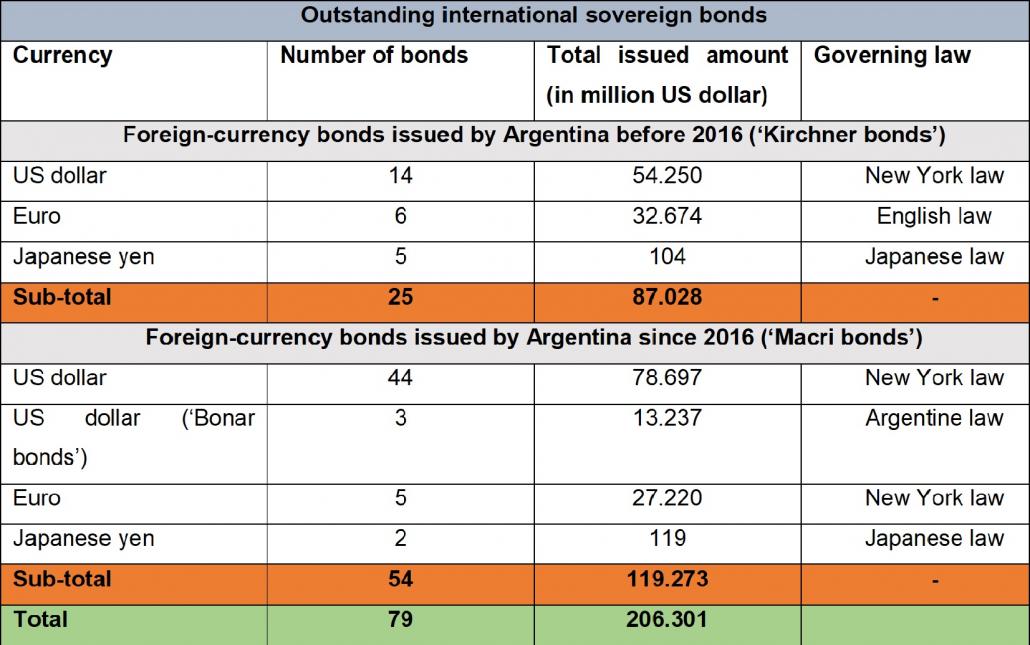

International sovereign bonds

The bulk of Argentina’s international sovereign bonds (debt denominated in foreign currency) was issued in or after 2016, given that Argentina settled much of its foreign-currency bond indebtedness that year. In total, the amount of outstanding international sovereign bonds is approximately $206 billions. Since the Macri administration took office in 2016, Argentina has issued a total of 54 new international sovereign bonds with a total issued amount of $169 billion, under three different currencies (US dollar, euro, Japanese yen) and three different governing laws (New York law, Argentine law, Japanese law).

Source: Bloomberg

IMF loans

On June 20, 2018, the IMF Executive Board approved a 36-month Stand-By Arrangement (SBA) for Argentina with an amount of $50 billion, which was expanded on October 17 to a total amount of $57 billion. The fund completed its Fourth Review in June 2019, allowing the disbursement of another $4.3 billion, bringing total disbursements since June 2018 to $44.1 billion, equaling more than three quarters of the amount available under the SBA ($57 billion).

Legal Aspects and “Restructurability” of the Debt Stock

Domestic debt

Argentina has issued a significant amount of bonds governed by local law, many of them with relatively short maturities. The reprofiling or restructuring of local law bonds, can rarely be successfully challenged in court—not least since domestic judges tend to be more sympathetic to the government’s interests. Moreover, Argentine local-law bonds include none of the creditor protection clauses that are typical for sovereign bonds issued on international markets, such as collective action clauses (CACs), negative pledge clauses, cross-default clauses, or pari passu clauses. This means that a potential restructuring of Argentina’s international sovereign debt would not trigger any rights to accelerate domestic bondholders, and vice versa.

International sovereign bonds

Governing law

The majority of Argentina’s outstanding international sovereign bonds are governed by New York law. This being said, as Table 1 above shows, a significant amount of euro-denominated debt issued before 2016 is governed by English law.

Collective Action Clauses (CAC)

Given that both maturity extensions as well as haircuts on principal or coupon repayments require contractual changes, Argentina will need to hold a bondholder vote under the respective collective action clause (CAC) procedures laid down in Argentina’s various bond prospectuses. CACs allow a country to call a bondholder meeting and let a supermajority decide on a debt restructuring proposal by the country. In this context, the following issues will be relevant in a debt restructuring: (i) the existence of different CAC models in Kirchner and Macri bonds, respectively, (ii) pooling options, and (iii) the uniformly-applicable requirement.

First, one complication relates to the fact that Argentina has some legacy bonds outstanding that were issued in the debt exchanges in 2005 and 2010, respectively. The CACs in the bond issued pre-2016 (‘Kirchner bonds’) have different voting thresholds than the bonds issued after 2016 (‘Macri bonds’). While Kirchner bonds require affirmative votes of 85 percent of bondholders across all series as well as 66⅔ percent in each individual series, Macri bonds allow for a single-limb modification that require only one affirmative vote by 75 percent of bondholders across all series. In a wholesale restructuring Argentina will thus have to consider the different voting thresholds and should seek to anticipate holdout tendencies in Kirchner bonds.

Second, as recommended by the new ICMA Model CAC, the Macri bond prospectus allows Argentina to ‘designate which series of debt securities will be included for approval in the aggregate of modifications affecting two or more debt securities.’ This provision is also referred to as a ‘pooling clause’, as it essentially enables the issuer to sub-aggregate certain series of bonds into various voting pools, in which at least two different series must be pooled together. By putting apples in one basket (eg bonds with 3-4-year maturities) and pears in another (eg bonds with 25-30-year maturities), a larger crowd of investors may be willing to vote in favor of the debt restructuring. Voting takes place exclusively within the pools, and, besides the requirement to disclose the design of the various pools, there are no legal limits for the issuer as to the pools’ structure. The success of pooling is predicated on the bondholders’ approval—when it comes to pooling, the biggest obstacle will thus not be legal but transactional.

Third, the CACs in Argentina’s debt stock stipulate that restructuring offers made by Argentina to bondholders needs to be uniformly applicable to holders of debt securities affected by the modification. Generally speaking, the uniform applicability concept does not require equal Net Present Value (NPV) reductions but rather offering investors (i) the same new instruments or (ii) new instruments from an identical menu of voting options. Ultimately, calibrating the uniformly applicable requirement in a litigation-proof fashion will be the crux of any Argentine debt workout operation.

Pari passu clauses

The pari passu clause in Argentina’s old New York law bonds played a central role in what the Financial Times considered the “sovereign debt trial of the century”. All Macri bonds, however, feature the new ICMA pari passu clauses, which expressly reject the interpretation that the New York courts entertained. To be sure, the pari passu clauses in the Kirchner bonds are remarkably similar to the clause that holdouts successfully leveraged against Argentina in New York courts in the NML v. Argentina case.

What should speak in Argentina’s favor is the fact that, in October 2019, the Second Circuit has effectively overturned its previous pari passu decision and stated that a sovereign only violated the pari passu clause if acted in a ‘uniquely recalcitrant’ manner. It will not violate this clause if it simply pays some creditors and not others (selective default).

Official-sector debt

IMF loans

In its function as an official-sector creditor and lender-of-last-resort to sovereigns, the IMF enjoys de-facto preferred creditor status (PCS). Thus, while the IMF’s Articles of Agreement make no reference to the fund’s PCS, states have accepted the IMF’s de-facto priority for decades. Indeed, rather than a legal challenge, reneging on IMF debt is likely to trigger vigorous political reactions from the IMF’s members and may thus severely erode the international community’s willingness to provide further financial assistance to the country in distress.

A longer version of this post is available here. This post has previously been featured by the Columbia Law School Blue Sky Blog, and is also available here.

Dr. Sebastian Grund is an LLM student and research assistant at Harvard Law School and a former legal adviser to the European Central Bank.

Share: