As stablecoin products are being regulated in order to enter mainstream markets in the US, EU and UK, a key question debated in the regulatory fray is whether stablecoin products should be allowed to pay interest to holders. The industry lobbies for this while the banking lobby fiercely opposes. Is this a matter of contest between industry interests or is there a principled approach behind the prohibition against remuneration, which is the position largely adopted by the US (Genius Act), EU (Markets in Crypto-assets Regulation) and UK (BOE and FCA).

To answer the question, one must first appreciate financial regulators’ long-held distinction between bank-based financial intermediation and non-bank financial intermediation in order to understand where stablecoins are positioned for regulatory classification purposes. Regulatory categories or boundaries can change, but drawing upon my previous works, this opinion examines the case and what the position should be for stablecoin issuers.

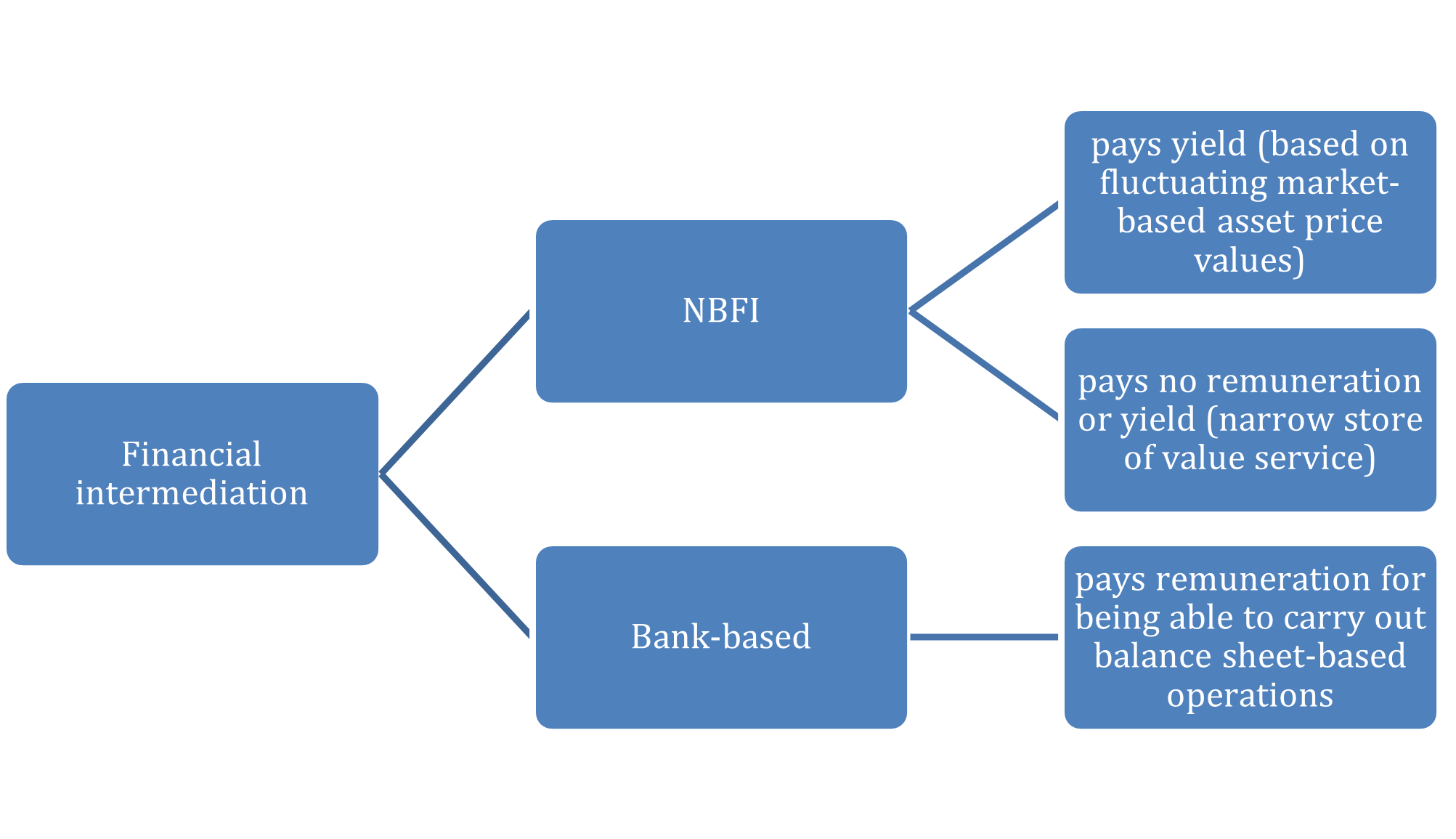

Bank intermediation is balance sheet-based and the management of bank solvency is crucial to the micro stability of the bank and wider systemic stability concerns. Despite the risk of bank insolvency, depositors’ claims against banks have been treated as good as money. This has not always been the case and has evolved from a long history of bank regulation. Banks predate central banks, and have been historically engulfed in financial stability episodes following from discount on claims against them and depositor runs. Bank regulation, central bank supervision and central banks’ monetary policy roles have together maintained a nexus of financial and monetary stability for broader economic stability. Given the large footprint of bank intermediation globally, it is neither practicable nor efficient for central banks to supplant them as money suppliers (and even topical developments in central bank digital currencies show limits in this ‘supplying’ role), despite the public good in preserving the stable value and singleness of money. Hence, banks act as ‘finance franchisees’, being regulated for stability purposes to underpin public trust in the value and singleness of money, supply money to the economy through credit, and facilitate money transfers through payment systems.

In contrast, non-bank financial intermediation (NBFI) is not balance-sheet based. NBFI manages entrusted capital, typically geared towards risk and yield. Money received for such intermediation (eg, investment) may be subject to loss of capital value, as well as being eligible for gains in capital value. In this manner, non-bank financial intermediaries are not regulated towards preserving the value of money as such, although they are regulated for other market stability concerns, even if there may be proprietary exposure in some arrangements.

The distinction between the two models can give rise to the following principles. First, balance sheet-based intermediation should not implicate depositors’ capital risk, hence giving rise to concurrently offering a store of value service. This means that bank regulators focus on banks’ solvency risk to preserve the value stability of money claims and systemic financial stability. A corollary of this reasoning is that remuneration need not be paid to depositors, as a store of value business model is not necessarily designed to provide a reward for depositors. The regulation of financial intermediaries involved in risk and yield generation addresses a different set of risks, in terms of anti-misselling to investors unless they are clearly informed of their value risks; and in terms of conduct of business in order not to harm investors’ reasonable risk and yield expectations.

However, industry practice renders the distinction not clearly perceived. Banks pay remuneration, albeit minimally at times, in return for depositors’ funding, their contribution to banks’ liquidity management and to maintain the inflation price-adjusted value of money stored with them. Banks paying remuneration to depositors should nevertheless not be treated in the same manner as yield-generation for non-constant asset value products. Regulators also arguably allow the distinction to be blurred. For example, holders of interests in money market funds could, before the global financial crisis 2007-8, enjoy treatment of claims against these funds to be as good as money, although their net asset values may diverge from par. Non-bank financial intermediaries such as alternative investment funds engage in both balance sheet-based and client asset-based intermediation.

Hence, when the fintech industry arose in the 2000s to disintermediate store of value and payment services from balance sheet-based intermediation, regulators faced the dilemma of whether to promote the innovative industry or to stultify it with the extension of the full gamut of bank regulation. Regulators in the EU and UK opted to create space for innovation without imposing excessive regulatory burdens. This is arguably the correct approach as the bundling of balance sheet-based intermediation with store of value and payment services has led to oligopolies which have become rent-extracting and uncompetitive—a situation ripe for the digital disruptions introduced by fintech.

A unique regulatory space was created: e-money services and payment services providers that are not banks should not engage in balance sheet intermediation in order to avoid stringent bank-like solvency regulation. Their store of value and payment services are therefore framed within the NBFI side of the distinction, which explains the regulatory tenet for reserve regulation backing e-money issuances and the segregated nature of reserves that are insolvency-remote from the firm. The obligation to redeem at par value is more akin to the ‘deposit’ characterisation. Ultimately, they are prohibited from paying interest to customers, which at first blush, settles on the bank-side of the distinction. This has created a ‘third regulatory category’, arguably obfuscating the banks and NBFI distinction. Stablecoins are placed in the same regulatory category.

This post argues that the ‘third regulatory category’ is situated within the broader universe of NBFI and is distinguished from balance sheet-based intermediation, which is the core business model for banks. The third regulatory category is one of narrow banking but without a banking franchise. This post argues that the case for paying either yield or remuneration is not made. The store of value business model neither carries out balance sheet-based intermediation (for which remuneration is paid to funding depositors) nor is the proposition to offer asset price fluctuations for yield-generation. It may have been unhelpful to make reference to ‘interest’ in e-money and stablecoin legislations, which attracts the comparison to banks. The prohibition against paying interest should be understood as articulating a lack of basis to either pay remuneration or yield. This is also a policy choice to prevent bank disintermediation, which may reduce the supply of credit to the economy.

Stablecoin issuers do not object to regulatory legitimacy. However, they seem discontent to be placed in the third regulatory category. It is acknowledged that the regulatory categorisation arrived would be perceived as restrictive in relation to the freedoms stablecoin business models have hitherto enjoyed in permissionless blockchain economies. Stablecoins are bearer digital tokens that purport to serve store-of-value functions for cryptocurrency holders. They allow cryptocurrency holders to convert quickly to native cryptocurrencies of permissionless blockchains so that they can avoid protracted periods of direct cryptocurrency holding, which exposes them to volatility problems. Increasingly, stablecoins are being used as collateral for borrowing or swapping between crypto assets in order to engage in yield farming, and both cryptocurrency exchanges and decentralised finance applications pay interest/yield on stablecoins locked as collateral. Cryptocurrency holders also tolerate slight deviations from par for stablecoins as they are traded in secondary markets and not usually redeemable directly with issuers. In this manner, stablecoin issuers may, due to the new regulatory characterisation, be unable to continue their investment yield-generating models as well as their business models for cryptocurrency holders.

My earlier work has shown that, so far, stablecoin regulation does not necessarily fit and cater for unregulated stablecoins’ business models. Stablecoins have enjoyed their ‘best of both worlds’ characterisation as money (relatively) and yield-generating product in the crypto economy, as they perform relatively better than the volatile native cryptocurrencies of their respective permissionless blockchains. This advantage is inapplicable to the mainstream economy, which is supported by institutions for the value stability of money. Regulation is a game-changer for stablecoin issuers’ business models. The perception of regulatory cleavage by stablecoin issuers is heightened as banks develop tokenised deposits which are increasingly being mobilised as tokenised bearer money- what stablecoins purport to be. Although tokenised deposits do not attract the narrow banking regulatory treatment, they are captured within the overall umbrella of bank solvency regulation, which remains stringent. If stablecoin issuers wish to pay remuneration and benefit from deposit guarantees, they would have to consider whether to enrol on bank solvency regulation. Such a strategic choice has been made by fintechs such as Zopa and Revolut, which have successfully obtained UK banking licences. E-money fintechs such as Wise seem to regard this trajectory as attractive. In the alternative, stablecoin issuers could reframe themselves as floating net-asset value products akin to money market funds, in order to pay yield to mainstream investors, while maintaining the niche position of providing on/off ramp access to cryptocurrency, an advantage stablecoins uniquely enjoy.

Hence, it is not that regulatory characterisation for stablecoin issuers is unfair compared to banks. If they disagree with being in the third category, it is up to them to clarify what the nature of their financial intermediation is. There are hazards for financial products to tout themselves as having both the qualities of money instruments and investment yield-generating instruments in the mainstream, an anomalous area occupied by some money market funds until the GFC, which exposed the unsustainability of this schizophrenic financial character. As my paper shows, stablecoins’ niche position remains in the crypto economy, being able to directly support onchain activities and serving as a relative store of value and investment anchor for crypto financialisation. This is a territory that tokenised deposits are unlikely to follow due to the need to adhere to regulatory tenets for payment services, such as settlement based on central bank reserves and finality for transactions underscored by a public good infrastructure. The unique business case for stablecoins should attract its regulation as a mainstream investment and not a money product, even if onchain participants treat it as relative money. This is no different from accepting that cryptocurrencies have become ‘assets’, not ‘money’ in the mainstream, even if in an onchain context, they can be accepted by blockchain participants as performing a payment function. A mainstream investment product is able to pay a yield while its backing net asset value would not be expected to be constant.

This does not mean that US-style securities regulation is the candidate for stablecoin regulation by default, as investment instruments of different types can be regulated differently. The EU and UK are maintaining offer regulation for stablecoin issuers, in addition to narrow banking regulation for them. This may be the ‘worst of both worlds’ for the third regulatory category. I argued for these bodies of regulation not to concurrently apply, but to apply along a spectrum depending on the stablecoin’s business uses, so that stablecoins serving as on/off ramp access to cryptocurrency and maintaining a relative (not absolute) pegged value may be treated along the investment end of the regulatory spectrum. The narrow banking end of regulatory framing can kick in if mainstream payment use increases, making the case for value stability needs. This may be a way forward for regulators and industry to become mutually responsive towards their respective objectives. Back to the question of whether stablecoin issuers should pay interest, the answer may be that regulators should let them choose whether to engage clearly with a remuneration-based or yield-based business model, but minding the different applicable regulatory consequences.

The author’s most recent articles related to this piece are available here and here.

Iris H-Y Chiu is Professor of Corporate Law and Financial Regulation at the University College London Faculty of Laws.

Share: