Few issues in corporate governance have become as politically charged as environmental, social, and governance (ESG) policies. What began as a framework for integrating ESG factors into investment and risk analysis has, in recent years, turned into a broader ideological fight within the debate over corporate purpose, fiduciary duties, and the role of business in public life. In the early 2020s, ESG engagement was widely embraced by major asset managers and regulators as part of mainstream risk management. More recently, however, it has faced a sharp backlash in politics, legislation, administrative action, and litigation, with critics casting ESG considerations as a threat to shareholder value. At the same time, the regulatory debate over mandatory versus voluntary ESG disclosure has intensified, especially after the rise and fall of the US SEC’s climate disclosure initiative.

Our recent paper, The Hidden Benefit of ESG, forthcoming in the Harvard Business Law Review, offers a novel contribution to this debate. Instead of asking whether ESG engagement is normatively desirable, or whether ESG disclosure should be mandated as a matter of public policy, we ask a more concrete corporate governance question: can ESG metrics serve as measurable signals of a company’s internal discipline and oversight? More specifically, do companies with higher ESG scores also produce more reliable financial disclosure?

That question matters because much of the public debate about ESG frameworks tends to overlook a core feature of well-governed firms: their ability to generate accurate, trustworthy information for investors and markets. Even investors who are indifferent to sustainability as a normative goal should care about ESG performance if it helps identify firms that ‘run a tighter ship’.

To date, the literature has offered competing arguments, but no conclusive empirical evidence. Some studies find that ESG activities improve financial performance and thus reduce the need to manipulate reports; others warn that high ESG scores may serve as a smokescreen aimed at distracting investor attention from poor financial performance.

Our empirical analysis is based on a dataset of 2,386 US-listed firms over the 2016–2021 period (9,715 firm‑year observations in total), using MSCI ESG ratings as the measure of ESG performance and financial statement restatements as a proxy for financial reporting quality. Restatements are revisions made to previously issued financial statements to correct errors, omissions, or deliberate misstatements. Restatements are particularly useful in this setting because they are externally observable corrections of prior disclosure failures. Fewer restatements indicate higher reporting quality.

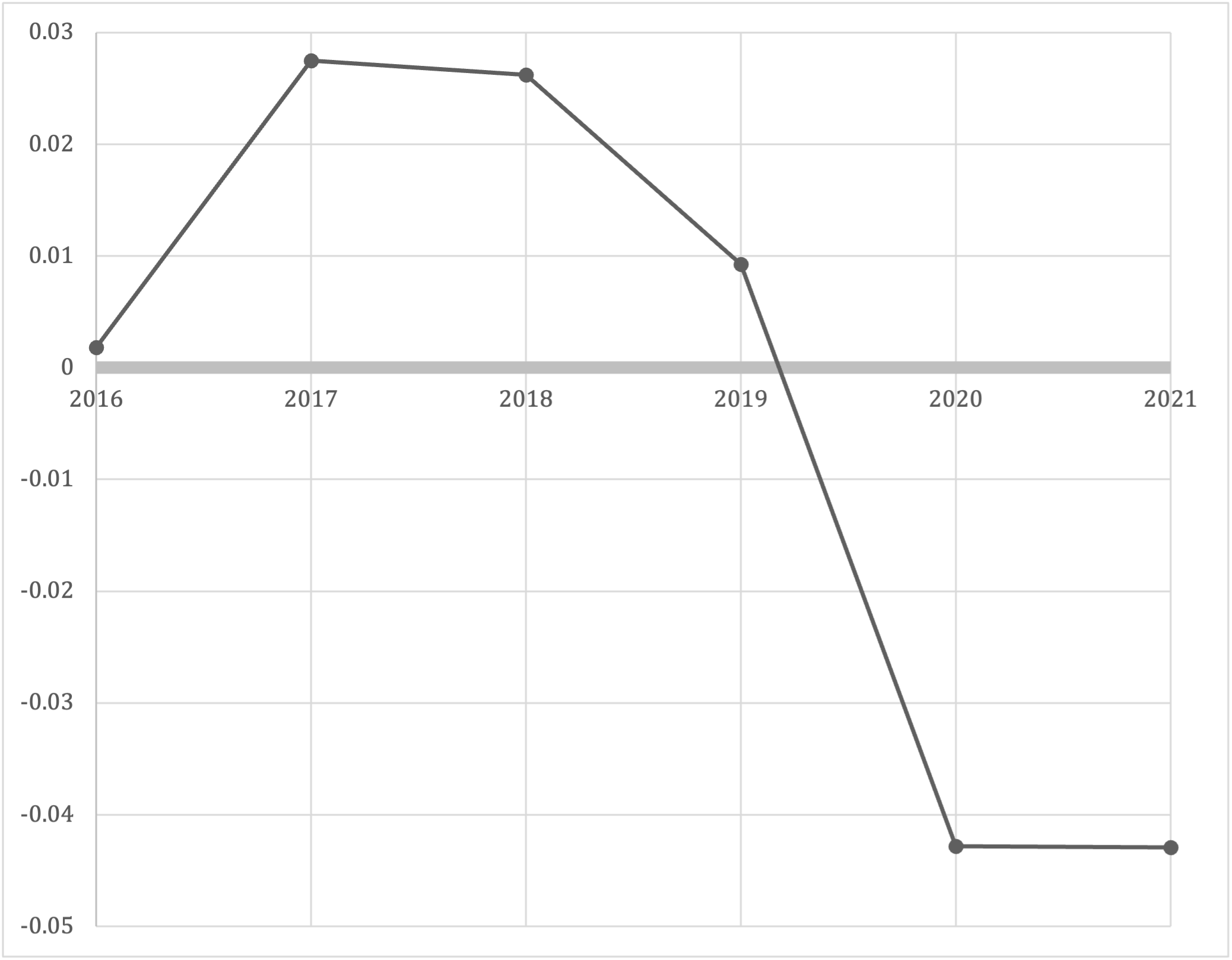

We find that mean ESG scores increased significantly in the aftermath of the 2019 Business Roundtable Statement on the Purpose of a Corporation (BRT Statement), signed by 181 CEOs of major US companies, including Amazon, Apple, Oracle, General Motors, and JPMorgan Chase. This Statement marked a shift from shareholder primacy toward a broader stakeholder-oriented approach, thereby effectively anchoring the integration of ESG considerations into corporate decision-making. Our results suggest enhanced corporate ESG engagement in the post-BRT Statement period.

We then use the BRT Statement as an exogenous, economy-wide shock to corporate ESG orientation. That design allows us to test whether, after this inflection point, higher ESG scores are followed by improved financial reporting quality.

Using the Pearson correlation coefficient to examine the link between ESG scores and the number of restatements, we find that, in the post-BRT Statement period, a statistically significant negative relationship emerges between ESG scores and the number of restatements. In other words, firms with stronger ESG performance are less likely to restate their financial statements.

These findings support a firm-level causal link between stronger ESG performance and more reliable financial disclosure. Our results suggest that the post-BRT Statement increase in ESG attention is not merely rhetorical but also carries a hidden benefit in terms of the integrity of financial reporting.

Our findings have significant policy implications. For investors, ESG scores can serve as useful signals of financial reporting quality, facilitating the identification of firms demonstrating superior financial accountability and transparency. For companies, ESG engagement is a governance tool that bolsters financial integrity and builds long‑term investor trust.

For regulators, our findings contribute to the ongoing debate on mandatory versus voluntary ESG disclosure. The analysis shows that private ordering, as evidenced by the impact of the BRT Statement, can produce real governance improvements. This suggests that regulators can design hybrid frameworks that combine baseline mandatory disclosure with room for voluntary, firm-specific ESG engagement.

Our results also matter for legislators and courts evaluating anti-ESG initiatives. In recent years, several US states have spearheaded anti-ESG laws aimed at curtailing the consideration of ESG factors in public investment decisions. We show that ESG engagement can be understood as a rational, data‑driven strategy to manage risk, rather than as a political agenda. Therefore, US states should be cautious in limiting ESG considerations if they wish to maintain robust investor protection and healthy capital markets. Moreover, our perspective provides courts with a basis for interpreting ESG measures as grounded in financial accountability and transparency.

The authors’ paper can be accessed here.

Dov Solomon is Professor of Law, College of Law and Business.

Ido Baum is Associate Professor of Law, College of Management.

Rimona Palas is Associate Professor and Head of the Accounting Department, College of Law and Business.

Dalit Gafni is Associate Professor and Dean, School of Economics, College of Management.

OBLB types:

Research

Share: