{kind=link}

The Application of the EU Markets in Crypto-asset Regulation to Decentralised Finance

Posted:

Time to read:

2 Minutes

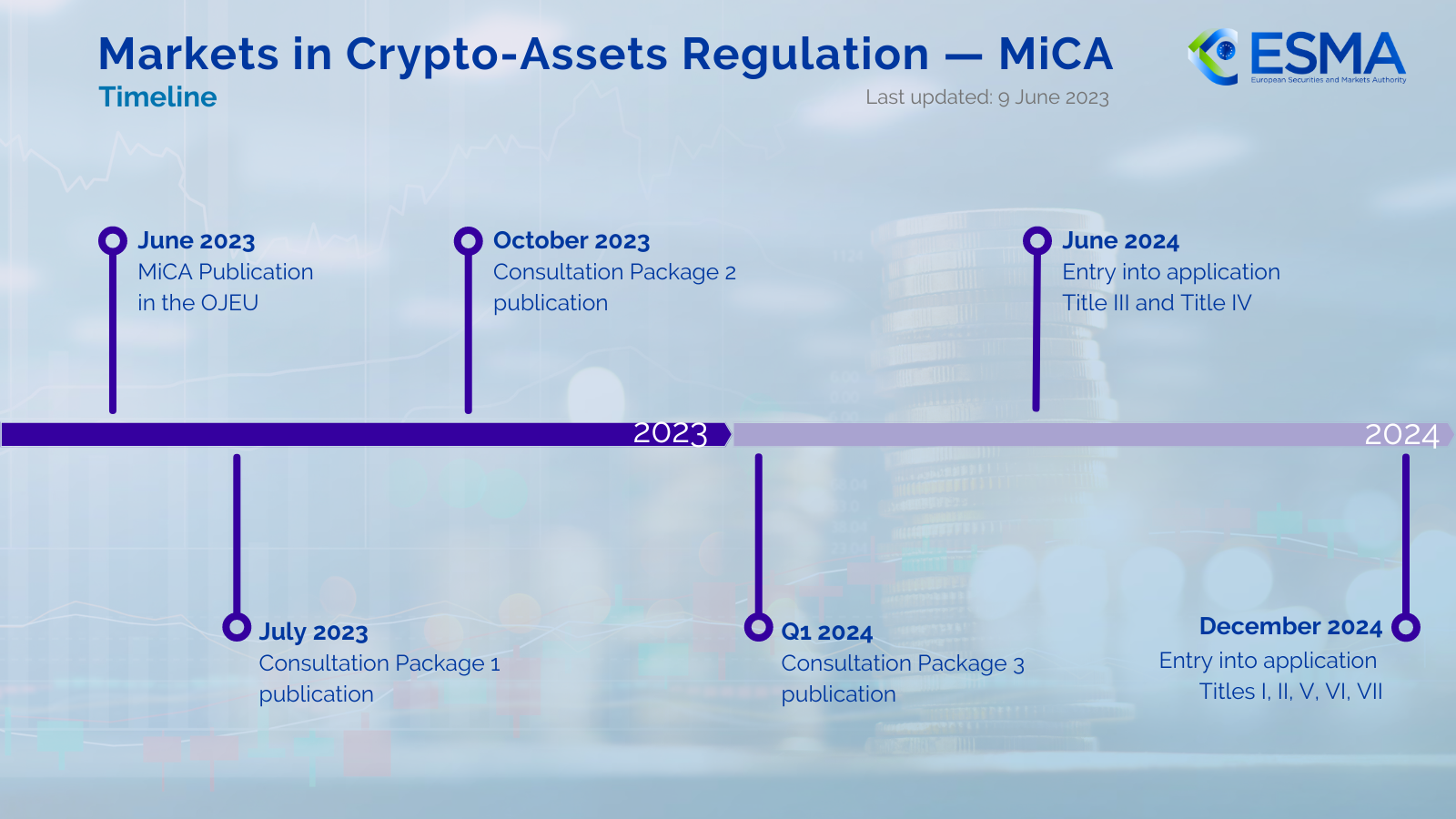

The Markets in Crypto-assets Regulation (MiCA) has been passed by the European Union in June 2023. This Regulation will come into effect from the middle of 2024 to the end of the year. The Regulation affects offers of utility tokens made in the EU, as well as asset-referenced stablecoins and e-money tokens issued in the EU, and a range of crypto-asset service providers.

There exists plenty of commentary and literature on the main coverage of the Regulation. My paper has instead a narrower focus, namely on whether and to what extent the Regulation applies to decentralised finance (DeFi) applications that are peer-to-peer in nature. These applications have been developed in vast numbers on the popular Ethereum blockchain and other permissionless blockchains such as Polygon and Solana. They allow ‘financial’ functions to be carried out on crypto-assets and are used extensively by crypto-asset holders to hedge, invest and generate yield on their crypto-assets.

The article first discusses DeFi as pooled applications to which an individual crypto-asset holder contributes, usually locking up one’s crypto-asset in exchange for another one that is subject to the pool’s algorithmic rules. These rules provide incentives for yield earning and generation for contributors, and often also allow contributors to participate in the developing governance of the application. Although such applications conceive of the ultimate empowerment of anyone to participate in financialisation activities without being subject to a financial intermediary’s rent extraction, these applications are not peer-to-peer in nature but peer-to-pool. Pool governance is subject to the usual governance problems in groups or organisations, ie concentration of power, potential abuse of power and self-interested motivations.

A subsequent question arises as to whether MiCA Regulation applies to DeFi applications and, in consequence, whether regulatory standards resolve the issues generated by DeFi, which at present revolve around user risks rather than financial stability. In that sense, the paper teases out the uncertainty as to whether DeFi applications would fall within the definition of a ‘crypto-asset service provider’. The paper highlights the high thresholds and lack of fit for DeFi’s authorisability, but also points out that technical standards issued by the EBA are beginning to classify some DeFi type applications, such as automated market makers, as crypto-asset service providers operating a trading exchange. Further, authorisation conditions are not compatible with DeFi’s envisioned model for organic governance to develop, while tolerating the emergence of governance scandals and problems.

Nevertheless, being caught within the scope of the Regulation does not necessarily mean that regulation over DeFi is either appropriate or optimal. Indeed, if MiCA is extensible to DeFi but fits awkwardly with DeFi business models, the market for DeFi applications in the EU could be strangled by MiCA’s application, paving the way for centralized types of crypto-financial intermediaries (which are comfortably covered within MiCA’s scope) to gain major market share. In this manner, there may be a case to argue for a regulatory update that works with DeFi’s innovative features while governing the precise risks they give rise to.

In interrogating the question of whether MiCA applies to DeFi, we uncover broader issues that require policy-makers’ attention. One is that comprehensive EU-level harmonisation that provides regulatory regimes for new developments face challenges in relation to catching up with changes, and the technological neutrality of regulation cannot be regarded as a given or as easily achieved. Secondly, MiCA’s application or otherwise to DeFi may not answer the question whether DeFi is appropriately governed or regulated. This is because the risks from DeFi may be financial in nature, but highly bound up with governance risks that flow from its a-legal decentralised autonomous organisation (DAO) form. There is ultimately a need to address policy-makers’ response to the development of DAOs that attempt to ‘house’ developmental projects without being subject to legal organisational rules. This area, although at a meta-level above the specific sectoral regulation in finance, should not be developed exclusively without the consideration of financial regulation objectives. The policy implications for DeFi and their DAO housing increasingly reflects the interrelation between financial regulation and other areas of policy and regulation, whether general or specific.

Iris H-Y Chiu (hse-yu.chiu@ucl.ac.uk) is the Professor of Company Law and Financial Regulation at University College, London.

Share: