Our paper ‘Why “Less is More” in non-Financial Reporting Initiatives: Concrete Steps Towards Supporting Sustainability’ sheds light on why ‘less is more’ in the non-financial reporting landscape and explains how an effective decluttering of the non-financial reporting landscape can take place by focusing on improving and widening the scope of the application of the EU Non-Financial Reporting Directive.

Knowing ‘the price of everything and the value of nothing’ is more than just a nice turn of phrase that Oscar Wilde had Lord Darlington quip in one of his plays. Projecting into the future, the phrase has spoken volumes on how modern society has drifted away from cultural values and has also highlighted society’s collective failure to place those values on a par with financial ones. Yet in the area of corporations’ non-financial reporting the problem remains that, although in the year 2020 we have reached a common ground on the fact that sustainability is a value worth preserving, there is no rate, no metric, no price nor cost attached to it, which arguably creates chaos for private and public actors alike. The fact that sustainability cannot be accounted for in a consistent way is the essence of the problem. Assuming that the chaotic framework for non-financial reporting is part of the problem, we argue that fixing that framework must be part of the solution.

What was the case for introducing non-financial reporting in the first place?

For years governments have taken solace in the idea that corporations' transparency on their corporate activity in relation to sustainability through voluntary reporting is adequately addressing the problem. It is evident however that in practice non-financial reporting is failing to deliver truly sustainable results. In our paper we discuss why this is the case and what can be done about it. How does the varied reporting landscape in the field of non-financial reporting impede the objectives of fostering corporations' sustainable practices? Which initiative, among the options available, may best meet the sustainability objectives after a decluttering of the landscape takes place?

Why is this issue topical and of significance?

Climate Crisis. Corporate contribution to climate change is so clear that it merits policy makers' primary attention in terms of prompting corporations' efforts to reduce global warming and carbon emissions. Industrial activities of corporations of all sizes provide the link between human action and global warming. This is documented by authors such as Wright and Nyberg who observe in their book Climate change, capitalism, and corporations (Cambridge 2015, at 3) that corporations are the ‘principal agents’ of greenhouse gas emissions. Certain companies in particular have been identified as responsible for emitting nearly two-thirds of industrial carbon dioxide and a small number of carbon producers are responsible for methane emissions, contributing to a rise in atmospheric concentrations of CO2 and CH4, GMST and global sea level (Heede et al 2014). One recent report, for example, warns that there are only 12 years left to act meaningfully in order to avoid catastrophic levels of global warming with corporations having played a central role in bringing about this global warming threat (IPCC Special Report—Global Warming of 1.5ºC 2019 Report).

Response. In response to the impact of corporate activity on the environment and on society, multiple initiatives have been developed to encourage or demand that companies report on their activities. Such initiatives, voluntary and mandatory, operate largely on the assumption that, if a company’s activities are opened up to the world, their impacts can then be measured, stakeholders can judge how beneficial or harmful they are and shareholders can decide if they are the right companies to invest in. Arguably, the most comprehensive mandatory legislation is the European Non-Financial Reporting Directive which was adopted in 2014 and has since been implemented in Member States across the European Union. Applying to large public-interest companies with more than 500 employees, such undertakings are required to provide a non-financial statement containing information to the extent necessary for an understanding of the undertaking's development, performance, position and impact of its activity, relating to, as a minimum, environmental, social and employee matters, respect for human rights, anti-corruption and bribery matters.The general aim of the Directive of 2014 is three-fold: i) to improve the quality of non-financial reporting across the EU; ii) to allow greater comparability; and iii) to attract inward investment. More specifically, as provided for by the Directive itself, its objective is ‘to increase the relevance, consistency and comparability of information disclosed by certain large undertakings and groups across the Union’ and essentially aims for non-financial information published by undertakings to become more consistent and comparable. However, companies that do not have policies on the subject matters identified may choose to provide minimal disclosure through the Directive’s comply or explain format, requiring them only to explain why they do not have such policies in place. The flexibility and discretion given to undertakings in what and how they disclose does little to improve consistency and comparability in reporting across the corporate sector. Reform is on its way. Steps are being made in the right direction towards clarifying metrics around sustainability as addressed in the White Paper by the World Economic Forum published in January 2020, Toward Common Metrics and Consistent Reporting of Sustainable Value Creation. At EU level, proposals for reform are now likely to be forthcoming , following a consultation exercise by the European Commission that had commenced in January 2020.

Metrics. To support the function of the market towards sustainability, metrics are required. Unfortunately, market pricing is unlikely to reflect the sustainability of a corporation within its broadest sense since mandatory and systematic reporting of all relevant information on CSR practices is not yet required . One important area for reform therefore is to widen the target group and for initiatives to be steered by metrics that will help markets reveal unsustainable behaviour towards people and planet.

Excessive choice and purpose. The excessive choice offered to companies, in terms of what and how they will report in the sustainability arena, gives rise to serious problems from a behavioural economics perspective. The variety of choice of voluntary reporting in the context of sustainability leads to uncertainty surrounding the utility of the information corporations are required to provide. Referring to what is known as the ‘Sisyphus effect’, behavioural economics scientists investigate how the importance of finding purpose in any task influences labour supply and productivity (Ariely et al, 2008). Transposed to the area of sustainability reporting, the pointlessness of the task of non-financial reporting for most corporations easily explains companies' unwillingness to engage in this activity beyond compliance and a box-ticking exercise. The overabundance of choice and the quest for more meaningful reporting point to a need to clean up the existing non-financial reporting landscape by making the target recipients clearer, connecting the required disclosures more closely to their needs and clarifying what is meant by the concept of materiality for non-financial reporting purposes.

Too many initiatives in the non-financial reporting arena?

There exists a chaotic system of financial reporting, CSR reporting, non-financial reporting and integrated reporting. As a result, policy makers are falling far short of the objective of increasing comparability and credibility as they seek for companies to be held accountable and to behave in ways that do not harm the people and the planet. Why is this so? Sustainability continues to remain a contested concept and varied interpretations of the term are available. Variances between companies and industries in relation to how each is operating, sustainably or unsustainably, also continue to exist. Such variances have so far inhibited drafting tailored legislation to reflect the individual risks to global sustainability in an all-encompassing manner.

Why should we focus on the NFRD over other initiatives?

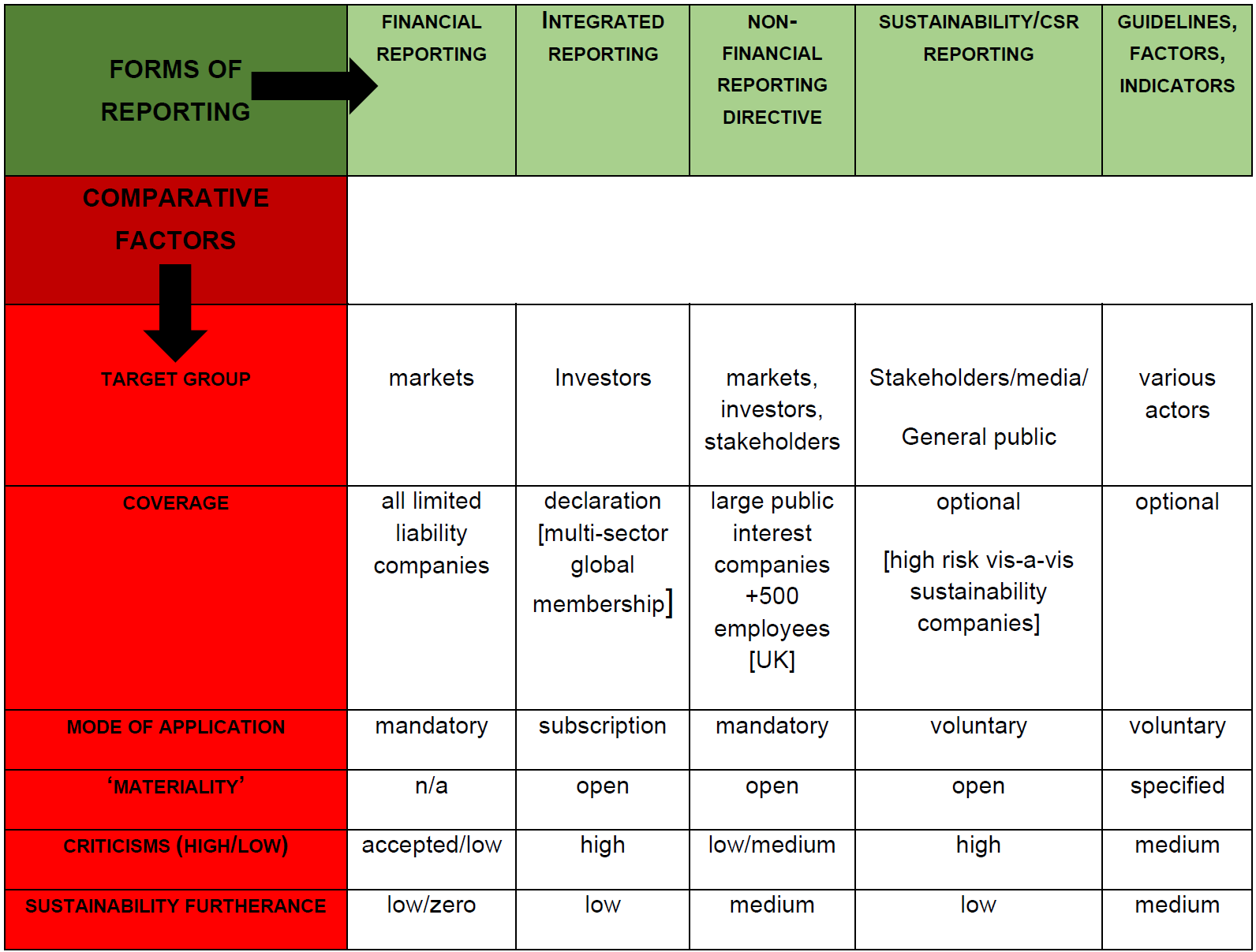

Our paper concludes that policymakers should focus their attention on reform of the NFRD for the purpose of realising an effective decluttering of the non-financial reporting landscape. The sources of data for the construction of the table below are provided from academic literature devoted to discussing the different initiatives, the primary source of the text of each initiative itself and reports on the application of each initiative following its adoption.

Table 1: Forms of Reporting Initiatives and Systematic Comparison

Despite its own limitations, the NFRD can be seen as ‘an important incremental step’ towards ‘mainstreaming sustainability reporting as mandatory rather than optional’ (Ahern, 2016). One of its major contributions is to inspire action by governments and individual entities it might be viewed as a catalyst to encourage more detailed and varied ways of bringing about corporate and stakeholder engagement in reporting and sustainability processes (Camilleri 2015).

Contribution and Conclusion

Random and arbitrary compliance with various initiatives makes companies’ sustainable practices ‘less’ rather than ‘more’ transparent. Our paper offers a comprehensive view on different reporting frameworks. It shows that there is a need to provide some clarity in this complex landscape. Fundamentally, the current reporting landscape is unlikely to impact positively on efforts towards sustainability. We suggest in our paper hat the scope of the NFRD, as the most promising of the existing initiatives, should be revisited so as to enhance its contribution to furthering corporations' sustainable practices. Our paper supports reform of the NFRD which has constituted a positive step in the right direction. What is required now is stronger guidance on what to report and how to report it. Steps are being taken in the right direction towards clarifying metrics around sustainability (World Economic Forum 2020). A standardized and streamlined framework is necessary in order to pin companies down to something more concrete, rather than giving them too much choice on which guidelines, frameworks or recommendations they may opt to follow. Stronger, clearer and more concrete definitions of key concepts are required, as well as clarification of the rights of stakeholders in this area of activity. Proposals for reform that have arisen, with a consultation exercise by the European Commission, (European Commission Consultation 2020) are therefore to be welcomed. We suggest an expansion of the NFRD’s scope and that it represent sustainability as a positive instead of reducing the focus only to negative risks. EU member states and companies should have opportunities for effective compliance with the reporting requirements, with the NFRD better defining the concepts it refers to.

Georgina Tsagas is a Senior Lecturer in Private and Commercial Law at Brunel University Law School.

Charlotte Villiers is a Professor of Corporate Law at the Bristol University School of Law.

OBLB types:

Research

Share: